The global payment scene has never been this competitive or complex.

People from all regions expect a seamless experience across currencies and devices. And using a single transaction gateway no longer makes sense.

Payment orchestrators make multi-provider transaction infrastructure possible. Hence, choosing the right payment orchestration solution is important.

Merchants are embracing the payment authorization platforms with open arms, as the market grew from $9.32 billion in 2025 to $10.39 billion in 2026 and is projected to grow at a CAGR of 12.02% to $20.65 billion by 2032 (Source).

Businesses are turning to them, whether they be scaling new markets, suffering from high decline rates, or just want to minimize processing fees. All of which directly impacts your bottom line.

In this article, I’ll break down these transaction orchestration platforms. The following sections answer why they are essential in 2026, what capabilities define a great one, and how to choose the right one that fits your business.

KEY TAKEAWAYS

- How people pay has changed a lot in 2026 and will continue to do so.

- Relying on a single transaction gateway is risky, hence they are embracing payment orchestration platforms.

- These allow multi-PSP support that reduces decline rates and transaction costs.

- Choose the one that fits your business model.

A decade ago, transaction orchestration was just an idea discussed by fintech enthusiasts. Now, all firms operating across various regions with a considerable transaction value are interested.

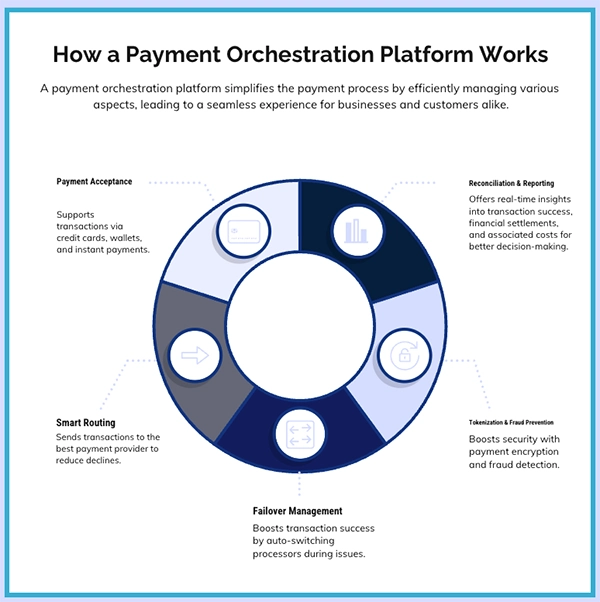

At its core, a transaction orchestration platform sits between your checkout and the broader ecosystem of banks, acquirers, alternative payment methods, and processors — acting as an intelligent layer that decides, in real time, how each transaction should be routed, retried, and recorded.

What has changed dramatically over the past few years is the sophistication of that intelligence. Early orchestration tools were essentially glorified routing tables. Modern platforms do something far more powerful: they analyze dozens of variables per transaction — card type, issuing country, transaction amount, time of day, historical performance of each provider — and make a routing decision in milliseconds that maximizes the probability of approval while minimizing cost.

The business case has become undeniable. Companies that have implemented mature orchestration infrastructure consistently report approval rate improvements in the range of 25 to 30 percent compared to single-provider setups. That number isn’t theoretical. It reflects the compound effect of intelligent routing, cascading fallback logic, and automatic card data updates working together. When you consider that the average cart abandonment rate at checkout already sits above 70 percent globally, even a modest improvement in payment approval can translate into tens of millions in recovered revenue at scale.

There’s also the cost dimension. Processing fees vary significantly between providers, and without orchestration, most businesses default to their primary acquirer for every transaction, regardless of whether it’s the cheapest or most likely to succeed. Smart orchestration eliminates that inefficiency, dynamically selecting the most cost-effective routing path for each transaction type and region. Businesses implementing this approach have documented processing cost reductions of up to 30 percent — a figure that compounds quickly as transaction volumes grow.

In 2026, the question is no longer whether to adopt transaction orchestration. It’s which platform will give you the most leverage.

Many of the orchestration platforms offer just basic routing; only some genuine ones provide a comprehensive payment infrastructure.

When evaluating platforms, these are the capabilities that should be non-negotiable:

A platform with 600 or more integrations gives you genuine global coverage — the ability to offer locally preferred transaction methods in virtually every market you enter, without building those integrations yourself. This matters not just for conversion but for market entry speed. Partnering with a platform that already has deep connectivity means you can expand into a new geography in days rather than months.

Equally important is what happens when a transaction is declined. Cascading logic should automatically retry through alternative channels within the same payment attempt, invisibly to the customer. This single feature can recover a significant portion of transactions that would otherwise be lost entirely.

When a card is reissued — something that happens constantly across any large customer base — automatic card update mechanisms ensure that recurring billing continues without interruption and without requiring customers to re-enter their details. The downstream effect on authorization rates is measurable: platforms with mature tokenization infrastructure consistently report authorization rate improvements of several percentage points.

Some platforms offer more than 150 individual parameters that businesses can tune to their specific risk profile. Critically, the best systems adapt to emerging threats automatically rather than requiring manual rule updates. Platforms built on decades of combined expertise in payment fraud carry a meaningful advantage here.

It also means supporting a genuinely broad range of currencies and payment methods, including cryptocurrencies, so that localization is a feature rather than a future roadmap item.

The best platforms handle transaction matching across all providers automatically, maintaining clean settlement records and surfacing actionable reporting without manual intervention.

The following infographic summarizes the capabilities and advantages of a great payment orchestration platform:

Okay, you have a list of good transaction orchestration providers, but the right one to choose still depends on your business model.

For businesses with significant recurring revenue, the priority should be on subscription management depth, tokenization quality, and automatic card update capabilities. Churn driven by failed recurring transactions is a silent revenue leak that orchestration can directly address. Look for platforms that offer flexible billing configurations, multiple retry logic options, and native support for tokenized wallet payments, including Apple Pay and Google Pay.

For high-volume transactional businesses — marketplaces, travel platforms, digital goods — the routing engine’s sophistication and the breadth of provider integrations will drive the most value. In these environments, even fractional improvements in approval rates compound into substantial revenue at scale. The ability to route by card type, issue region, and real-time provider performance is more valuable than any other feature.

For businesses entering new geographic markets, the integration library is the critical variable. Markets across Southeast Asia, Latin America, Africa, and the Middle East have distinct payment preferences and locally dominant methods that global card networks don’t adequately serve. A platform with genuine local coverage — direct integrations with regional acquirers and alternative transaction methods, not just resold access — will dramatically outperform one that’s primarily optimized for North American and European card transactions.

One dimension that’s often underweighted in platform evaluations is the quality of implementation support. Payment migration — moving transaction history, anti-fraud rules, recurring billing agreements, and merchant relationships from a legacy system to a new platform — is genuinely complex. The difference between a vendor that hands you documentation and walks away and one that actively manages the transition, handles integrations, provides training, and develops custom features alongside you is enormous. Businesses that have gone through major transaction infrastructure migrations consistently cite this support quality as one of the most important factors in their decision.

Time-to-value is another practical consideration that matters more than it appears in vendor presentations. A platform that requires months of technical integration before you’re processing live transactions has a real cost — in delayed revenue improvement, in engineering resources consumed, and in competitive opportunity missed. The fastest platforms in the market can have businesses processing transactions within five days of starting implementation, with new provider integrations developed and deployed within two weeks.

Payments are changing in 2026, and the trends for the future are more or less clear.

First, the number of transaction methods consumers expect to see at checkout is growing, not consolidating. Buy Now Pay Later, mobile wallets, real-time bank transfers, and locally preferred APMs are all gaining share alongside traditional card payments. Managing this complexity without an orchestration layer is increasingly untenable.

Second, regulatory and compliance pressure on payment data is intensifying across virtually every major market. Platforms that handle tokenization, data residency, and PCI compliance natively remove an enormous burden from internal teams — and reduce the risk of the kind of data incidents that can permanently damage consumer trust.

Third, the margin pressure on transactions is real. As more transaction volume moves to lower-cost alternatives and interchange fees come under regulatory scrutiny in various markets, the ability to optimize routing toward lower-cost channels becomes a meaningful competitive advantage. Businesses that have built smart orchestration infrastructure will consistently outperform those that haven’t on a cost-per-transaction basis.

Among the platforms addressing this moment seriously, Akurateco has built a particularly strong position. Their platform connects businesses to more than 600 payment providers, banks, acquirers, and alternative transaction methods through a single integration — covering over 200 currencies and cryptocurrencies with 99.95% uptime SLA. The combination of intelligent routing, cascading fallback, real-time fraud prevention built on 50 years of combined team expertise, automated reconciliation, and flexible deployment options across SaaS, on-premise, and cloud-agnostic models addresses the full spectrum of what serious payment infrastructure requires in 2026.

What distinguishes their approach beyond the technical capabilities is the implementation model: a dedicated account manager for each client, a track record of migrating businesses from legacy systems without disruption, and a five-day path to live processing. For businesses that have seen payment infrastructure projects drag on for quarters, that commitment to speed is meaningful. Real customers across PSP, fintech, and e-commerce verticals have documented moving from contract to live operations in weeks, with measurable improvements in approval rates and processing costs following shortly after.

Transaction orchestration has moved from a competitive advantage to the baseline requirement for any business operating at scale across multiple markets or payment methods. The platforms that will define the next few years of this space are those that combine genuine technical depth with the operational support to make complex migrations and integrations actually work in practice. As you evaluate your options, prioritize integration breadth, routing intelligence, fraud prevention sophistication, deployment flexibility, and the quality of the partnership you’ll get through implementation and beyond. The platform you choose isn’t just infrastructure — it’s a direct lever on your revenue.

Stripe, PayPal, Razorpay, Square, and Adyen.

It’s AI-driven and security-focused, with a great user experience through instant transactions.

AKA Four-party scheme involves: Cardholder, Merchant, Issuer (Cardholder’s bank), and Acquirer (Merchant’s bank).