Many individuals perceive financial security as encompassing far more than merely accumulating savings. It fundamentally involves ensuring the safety and well-being of their family members while simultaneously fostering the growth of wealth for future generations.

That’s where ULIPs come in. You’re not the only one who has ever wondered what is ULIP. A Unit Linked Insurance Plan, commonly referred to as ULIP, represents a sophisticated financial instrument that amalgamates the features of life insurance with investment opportunities linked to market performance.

This dual-purpose product is specifically designed for individuals who seek to achieve a balance between the growth potential of their investments and the security provided by life insurance coverage.

That’s not it, in this blog post, we are going to explore more layers of this segment and provide valuable insights to the readers.

Let’s begin!

Key Takeaways

Understanding how a ULIP works

Decoding why it is a good long-term investment

Looking at the ULIP calculator

Discovering its distinctive characteristics in comparison to traditional methods

How Does a ULIP Work

There are two parts to the amount you pay for a ULIP when you buy one. These are –

Insurance Coverage: A chunk of your payment goes towards life insurance. If anything happens to you during the policy period, your chosen beneficiary will receive either the guaranteed amount or the current value of the fund.

Investing in Market Funds: The remaining amount is invested in the funds you choose, whether that’s stocks, bonds, or a mix, depending on your long-term goals and how much risk you’re comfortable with.

Your returns on traditional insurance plans are set and often lower. A ULIP, on the other hand, lets you grow your wealth by investing in market-linked instruments. When the policy term is over, you can also switch between funds if your financial goals or risk tolerance change.

Intriguing Insights

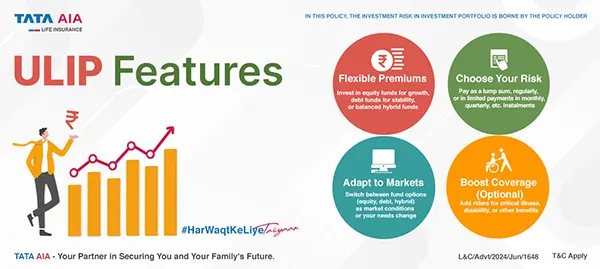

This infographic shows numerous ULIP features

ULIP as a Long-Term Investment Tool

ULIPs really shine when you look at how their value grows over time. Since most ULIPs come with a lock-in period of 5 years, they push you to stay invested. Once that period is over, that’s when the magic really kicks in. Putting your money in for 10, 15, or even 20 years lets it grow steadily, no matter if the market is having its ups and downs.

ULIPs are great for saving for big expenses like paying for a child’s college, building up for retirement, or creating an inheritance because they build wealth over time. They also, via their insurance component, cover your family financially if you pass away during the term of the policy.

Fund Switching Is A Unique ULIP Advantage

One of the cool things about ULIPs is the free fund switching feature. Imagine you’re young and ready to take some risks, so you pick a high-growth equity fund. Zoom ahead five years, and who knows, your goals might have shifted or the market could be a bit crazy. No stress! With ULIPs, you can smoothly switch from that equity fund to a balanced or debt fund without any tax headaches.

Premium insurance providers like Axis Max Life Insurance offer flexible switching options and smart fund management tools that help you optimise returns over time. This is something mutual funds or endowment plans do not allow without triggering tax consequences.

Interesting Facts After a Unit Linked Insurance Plan (ULIP) matures, the policy ends, and the insurer pays the accumulated fund value to the policyholder.

The ULIP Calculator Helps You Make Smart Plans

Before you buy a ULIP, it’s helpful to know what your returns might be over time. Using a ULIP calculator is super easy! All you have to do is enter a few basic details, like how much you’re putting in each month, how long you want your insurance to last, and what type of fund you’re interested in.

Once you do that, it’ll give you a ballpark figure of what your fund might be worth when you decide to cash out. A lot of insurance companies have online ULIP calculators that come with built-in scenarios that show what would happen with 6%, 8%, and 10% returns. This helps you stay ready and change your plans based on how the market is moving.

ULIPs and Tax Benefits of Triple Exemptions

Another reason why ULIPs have become a preferred choice among salaried professionals and young families is their tax-efficient structure.

Tax Component

Benefit Under Indian Tax Law

Premium Paid

Up to ₹1.5 lakh annually, under Section 80C, if you opt for the old tax regime

Sum Assured

Entirely Tax-free under Section 10(10D)

Fund Switching

No capital gains tax during fund switches within a ULIP

ULIPs not only boost your investment and provide insurance, but they also help you save on taxes every year and when the plan matures, as long as you stick to the tax rules.

ULIP vs Traditional Insurance and Mutual Funds

It’s common to confuse ULIPs with other financial products like traditional life insurance or mutual funds. But each serves a very different purpose.

Feature

ULIP

Traditional Insurance

Mutual Funds

Life Cover

Yes

Yes

No

Market-Linked Returns

Yes (Equity/Debt/Balanced Funds)

No (Mostly guaranteed or fixed)

Yes

Lock-in Period

5 years

10–20 years

No (but exit load may apply)

Fund Switching

Yes, without tax implications

Not applicable

Not allowed without exit or tax

Tax Benefits

Yes, under Sections 80C and 10(10D)

Yes

Yes (with limits and capital gains)

Transparency on Charges

High (clearly mentioned upfront)

Low

Medium

Who Should Consider a ULIP?

ULIPs aren’t for everyone since they require patience, long-term thinking, and a basic understanding of how markets move. But if any of these sound like you, then a ULIP might be worth considering.

Young professionals in their late 20s or early 30s looking to grow their wealth while taking care of their loved ones.

Parents who want to save up for future dreams, like their kid’s education, ideally over a 10–15 year plan.

Freelancers or business owners with unpredictable incomes who like the freedom to adjust their premium payments and switch funds as needed.

Tax-conscious investors looking to save under Section 80C (only under the old tax regime) while also enjoying the benefit of tax-free maturity, as long as their policy qualifies.

To understand exactly how much to invest and what kind of returns to expect, it helps to use a ULIP calculator again. Most people underestimate how much they’ll need for future milestones, especially with inflation, so using different values for premium and policy terms can help personalise your plan better.

Conclusion

If you’ve always treated life insurance and investment as two separate things, a ULIP might change how you look at financial planning. ULIPs enable you to create a more efficient and goal-oriented strategy by combining the safety net of insurance with the growth potential of market-linked funds.

Of course, like with any financial product, choosing the right ULIP depends on your needs, risk appetite, and time horizon. Providers like Axis Max Life Insurance offer flexible, digitally managed ULIP plans that adapt to your life goals; whether it’s buying a home, securing your child’s future, or planning early retirement.

Before signing up, compare the available ULIPs, review the fund options, understand the fees, and use a ULIP calculator to get a realistic picture.

Standard T&C apply

Insurance is the subject matter of solicitation. For more details on benefits, exclusions, limitations, terms and conditions, please read the sales brochure/policy wording carefully before concluding a sale.

Disclaimer: The content on this page is generic and shared only for informational and explanatory purposes. It is based on several secondary sources on the internet and is subject to changes. Please consult an expert before making any related decisions.

Tax benefit is subject to change as per the prevailing tax laws.

FAQ

What is the return of ULIP in 5 years?

A 5-year ULIP (Unit Linked Insurance Plan) return is not fixed but varies based on market performance and the fund type chosen, potentially ranging from 8% to over 12% annually in the last 5 years, with equity funds generally offering higher returns than debt funds.

Is ULIP a good or bad plan?

A ULIP can be better than an FD in some respects. For instance, it provides better returns and insures you under the same plan.

Is ULIP better than FD?

Yes, ULIPs are a better place to invest than Fixed Deposits. Apart from ensuring that your money is safe and providing you with life cover, they also give you a chance to earn by investing your money.